The company, which rejected BHP’s $43 billion second bid on Monday, is keeping its copper, iron ore and crop nutrients businesses. Anglo American owns three of the 10 most productive copper mines in South America, with plenty of room for growth. It is also a major producer of high-grade iron ore, which has historically accounted for the lion’s share of Anglo’s profits.

The company plans to reduce investment in its recently acquired fertilizer business from £1 billion ($1.26 billion) to £200 million ($251 million) in 2025. The next step will be to find strategic investors who can support the resumption of full-scale operations at the Woodsmith polyhalite project starting in 2026, CEO Duncan Wanblad said.

While the 107-year-old miner was already in the midst of its own asset review, the timetable had to be accelerated after BHP’s sweetened offer, Wanblad said. The overhaul, described by the chief executive as a “clear, compelling and decisive plan”, will unlock value for Anglo shareholders by creating a “radically simplified” company focused on “world-class assets”, he noted in a media briefing after the announcement .

“These actions represent the most radical changes at Anglo American in decades,” Wanblad added.

The Anglo boss said the miner would be “extremely highly valued” by the end of 2025, when the restructuring is complete, “to the point that if someone wanted to buy us at that particular point in time, they would have to pay a huge amount of money to do it .”

The sudden announcement was seen by some analysts as a strategy to attract interest from other potential buyers for the company’s secondary divisions and also to discourage aggressive takeover attempts by BHP.

“These assets that will be put up for sale will certainly appeal to competitors, some in whole (perhaps forcing a bid for the group, as BHP is trying before it breaks up on its own) and some in part,” Energy and Mining Quilter Cheviot analyst Jamie Maddock said in a note.

BMO analyst Alexander Pearce said Woodsmith’s cost cuts alone could be enough for a reasonable re-rating of Anglo American. “The intention to accelerate strategic change is likely to be well received, although the company will be less differentiated from competitors.”

Pearce noted that Anglo’s plans target $1.7 billion in cost savings from the new portfolio configuration, including $800 million in cost savings from the end of 2025.

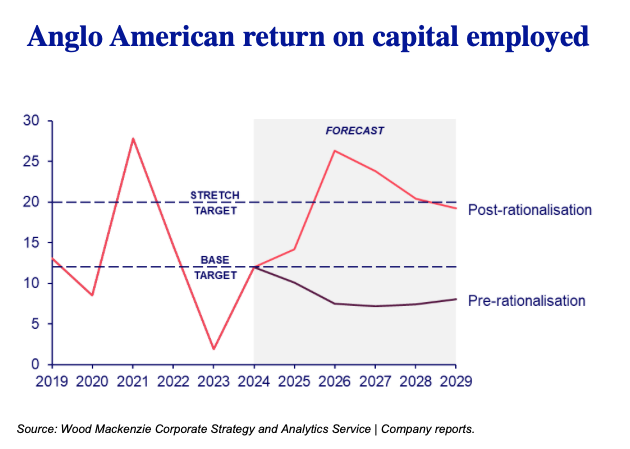

The move will transform Anglo from the most diversified to the most concentrated major miner, according to research firm Wood Mackenzie.

“We believed a major reshuffle of Anglo American’s portfolio was imminent,” said Wood Mackenzie’s James Whiteside, director of corporate metals and mining research. “But the choice to divest or spin off entire segments of its portfolio is consistent with the company’s new strategic priorities.”

Lost shine

De Beers, the world’s largest diamond producer by value, was founded in 1888 in South Africa by British mining magnate Cecil Rhodes. The company was part-owned by the Oppenheimer dynasty, which also founded Anglo American, until the family sold its 40% stake to Anglo American in 2012.

The diamond producer was the prized possession of Anglo’s vast business empire. He had a dominant position in the global gemstone market in terms of both overall sales and public perception due to the lasting impact of his 1940s “A Diamond is Forever” campaign.

The diamond sector, and De Beers in particular, has faced challenges over the past three years due to declining sales, a sluggish global economy and the rise of lab-created diamond alternatives.

Mark Wanblad said De Beers remains a “great business” and noted that the unit has already attracted interest from prospective investors, without naming names.

Anglo’s chief executive expressed confidence that the “structural problems” facing the diamond industry would be resolved. “There is no doubt that the structural problems that everyone is talking about will pass,” he said.

Market reaction

The company’s bold move could derail BHP’s plans to become a copper giant controlling about 10% of global metal production at a time when an urgent shift to a greener economy is pushing up both prices and demand.

Wood Mackenzie highlighted that iron ore and copper have been big cash generators for Anglo over the past five years, providing 58% of the company’s underlying earnings before interest, tax, depreciation and amortization (EBITDA).

“Looking forward, even without new investment, copper will overtake iron ore in terms of cash generation and this will allow Anglo American to use the proceeds to focus on brownfield growth in these core assets,” Whiteside said.

This was said by the South African Minister of Mining, Gwede Mantashe Financial Times that he would prefer Anglo’s restructuring plan to a BHP-led split and takeover. “I am happy with the rejection of the BHP deal and hope it goes ahead, after which Anglo can restructure itself to optimize shareholder value,” he said.

The minister’s support is crucial as it reflects the government’s position on the restructuring of a major player in the country’s mining industry.

The Church of England Pension Board, a UK asset owner and long-standing Anglo American shareholder, was also pleased with today’s announcement.

“We need more companies like Anglo that are ready to take advantage of opportunities to operate in emerging and developing markets like Africa, not less,” it said in a statement. “As a UK pension fund, we want the London Stock Exchange to remain a premium market for mining companies.”

Activist fund Elliott, one of Anglo’s 10 largest shareholders after amassing a $1 billion stake, is expected to issue a statement later in the day.

Ashwin Pillai, senior associate at law firm Charles Russell Speechlys, said the new plan responded to shareholder concerns about Anglo’s copper mines being undervalued by less valuable operations such as the diamond division. He also indicated there was still a chance BHP could increase its offer, potentially by including a cash component to make the deal more attractive.

Analysts believe Anglo American could easily gain $25 billion in asset value by selling or divesting (gross exit costs) its other commodities such as platinum, steelmaking coal and nickel over the next few years. For Wood Mackenzie, this represents a potential increase of $9.1 billion over the research firm’s underlying net asset value (NAV).

Experts warn that implementing Anglo American’s strategic plan will not be easy. By demonstrating a willingness to deconstruct the group, the company has given credibility to the proposed takeover by BHP, potentially making it more palatable to regulators in key markets such as South Africa, Wood Mackenzie’s Whiteside said.

Whiteside agrees that Anglo’s plan is undoubtedly bold, and losing the equivalent of 39% of 2024 profits would be transformative. However, the performance risk is significant and is borne entirely by Anglo American’s shareholders. If an increased offer from BHP materializes, it could be seen as a clearer option for shareholders.

“Anglo American’s strategic plan is undoubtedly bold, and shedding the equivalent of 39% of earnings to 2024 would be transformative,” Whiteside concluded. “However, the execution risk is significant and is borne entirely by Anglo-American shareholders, so if an increased offer from BHP materializes, it may be seen as an easier option for shareholders.”

Anglo American shares fell 2.8% to 2,632p by mid-afternoon in London, but recovered later to close 1.4% higher at 2,745p. That leaves the company with a market capitalization of $44 billion as of Tuesday evening.